If this message is not displayed correctly click here

|

Issue 546 - October 11th - 15th 2021 - Expressly created for 4.291 wine lovers,

professionals and opinion leaders from all over the world |

|

|

|

|

|

|

There are many unknown factors with which global trade, including wine trade, will have to reckon in the coming months. In the meantime, however, the latest ISTAT figures for the first 7 months of 2021, analyzed by WineNews, provide a real breath of optimism for wine exports. The recovery is solid, with a growth of +14.5% over the same period in 2020, reaching almost 4 billion euros in value: 3.98 billion euros to be precise. Better even than the first 7 months of 2019, when shipments of Italian wine abroad settled at €3.6 billion (+10.7%). |

|

|

|

|

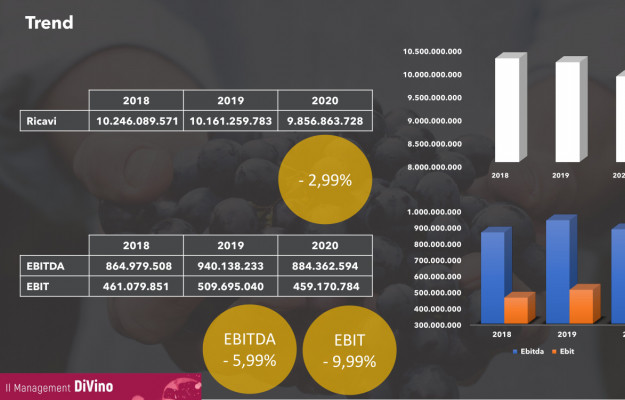

While the aggregate figures tell of a recovery of Italian wine on world and domestic markets that is in some ways formidable, in 2021, if we look at the balance sheets of the companies in detail, we discover that, in the end, it didn’t go so badly in 2020 either, at an overall level, given that, overall, revenues fell by just -2.9%, even if profitability suffered a little more, given that EBITDA fell by -5.9%. But the aggregate figure itself says something but not much, because, as is well known, the Italian entrepreneurial system is made up of very small companies and large companies, private individuals and cooperatives, farms and commercial enterprises, which, moreover, operate in many different areas. And so, looking in detail at the 2020 budgets, it is confirmed in black and white that, for some, 2020 was an even better year, from an economic point of view, than 2019. This was confirmed by the in-depth survey “What the balance sheets of Italian wine companies say”, presented by “Il Management Divino”, directed by Luca Castagnetti, (part of the Studio Impresa galaxy, part of the Reliant group), which not only took into consideration the balance sheets filed by 539 companies, 88% of those in Italy with a turnover of more than 3 million euros, but also divided them by turnover classes, types (private and cooperative, agricultural and non-agricultural) and other criteria. And so, at an overall level, it emerges that the panel’s revenues in 2020 were €9.8 billion compared to €10.1 billion in 2019, while profitability, or ebitda, was €884 million, lower than the €940 million in 2019, but higher than the €864 million in 2018, for example. Breaking down the figure, it emerges that the loss of revenue was mainly borne by private companies (6.1 billion in 2020 versus 6.4 in 2019), which, however, maintained a stable overall profitability ratio, on 11.3%, while cooperatives fell from 5.5% in 2019 to 4.9% in 2020. For small wineries under €5 million in turnover, profitability rose from 8.8% in 2019 to 9.4% in 2020, as well as for companies over €50 million in turnover, for which it rose from 8.9% in 2019 to 9.6% in 2020, while it was all the “middle ground” that suffered the most. |

|

|

|

|

The most important Italian wine fair is returning, though it will be in a different format, to ride the crest of the rebound that seems to be definitely solid for the sector after difficult months, physically and symbolically marking the restart. All this will be “Vinitaly Special Edition” in Verona, a “three-day” event (October 17-19) of business and services to accelerate the recovery of the sector on the main target markets and to take stock of the future of Italian wine also in the light of new purchasing and consumption trends. More than 200 buyers from 35 countries are expected in Verona, thanks to a highly specialized and profiled incoming campaign implemented by VeronaFiere and the Ice Agency, from markets such as the USA, China, the UK, Canada, Germany, Russia and more, together with more than 400 wineries - some of the most important in Italy - to toast to recovery. |

|

|

|

|

|

According to the analysis of the financial reports of “Il Management Divino”, looking at the levels of fixed assets of the companies, it emerges that those considered “light” (i.e. under a ratio between tangible assets and assets of 29.7%) have seen their ebitda grow from 10.1% to 11.4%, but once again mainly thanks to those under 5 million euros of turnover, which have gone from 8.6% to 13.3%, and those over 50 million euros, for which the parameter has grown from 11.5% to 14.4%. Those considered “strong”, i.e. those companies where ownership of vineyards and real estate weighs more heavily, on the whole, recorded an increase in revenues, from 2.1 to 2.5 billion euros, but lost something in profitability, which fell from 13.6% to 11.2%. Dividing again between agricultural and non-agricultural companies, however, it emerges that the “strong” agricultural companies recorded a slight loss in revenues and profitability between 2020 and 2019, while the non-agricultural ones saw revenues grow, but lost something in profitability. With two clear figures emerging: the “strong” agricultural companies were those with the best ebitda ever, with a rate of 19.15%. And looking at the territorial variable, those in Tuscany are ahead of everyone else, with an ebitda of 28.5%. |

|

|

|

|

|

From October 15, 2021, two great world wine territories, different but equally popular, one the land of the most prestigious declination of Sangiovese, that of Brunello di Montalcino, one of great Cabernet and Merlot, the Napa Valley, in California, will be officially twinned. Because at the conclusion of a process that has developed between Italy and the United States, the official signing of the twinning between the city of Napa and Montalcino will be staged, with the Italian, American and authorities of the two cities. |

|

|

|

|

Large-scale distribution, as is well known, has been the real lifeboat of wine consumption in Italy in the storm of the pandemic. Wine sales continue to grow in supermarkets, albeit much more slowly: in the first 9 months of 2021, +2% in volume and +9.7% in value (over the same period in 2020). This is confirmed by data from Iri research for Vinitaly, which will be presented in its entirety at “Vinitaly Special Edition” 2021 (at VeronaFiere, October 17-19). Data that, at the same time, confirms both the return to consumption away from home and the fact that purchases in supermarkets are increasingly directed towards higher-end wines, given that sales of DOC wine are growing by 4.8% and those of sparkling wines by 27%, but above all that values are growing much more than volumes. |

|

|

|

|

On September 30, 2021, there were 36.8 million hectolitres of wine in Italy’s cellars, 3% more than 12 months ago and 12.4% less than in July 2021, according to the report by the Ispettorato Centrale Repressione Frodi - Icqrf. 22% of national wine is in Veneto, 12.9% in Tuscany and 11.1% in Emilia Romagna. Despite the large number of GIs registered (526), the top 20 designations account for 54.9% of the total stocks of GI wines. Prosecco accounts for 6% of stocks, Chianti for 3.4%, Chianti Classico for 2.6%, Franciacorta for 1.9%, Barolo for 1.7%, Amarone for 1.4% and Brunello di Montalcino for 1.3%. |

|

|

|

|